Prometeia Atlante

Insight for your business

giuseppe.schirone@prometeia.com

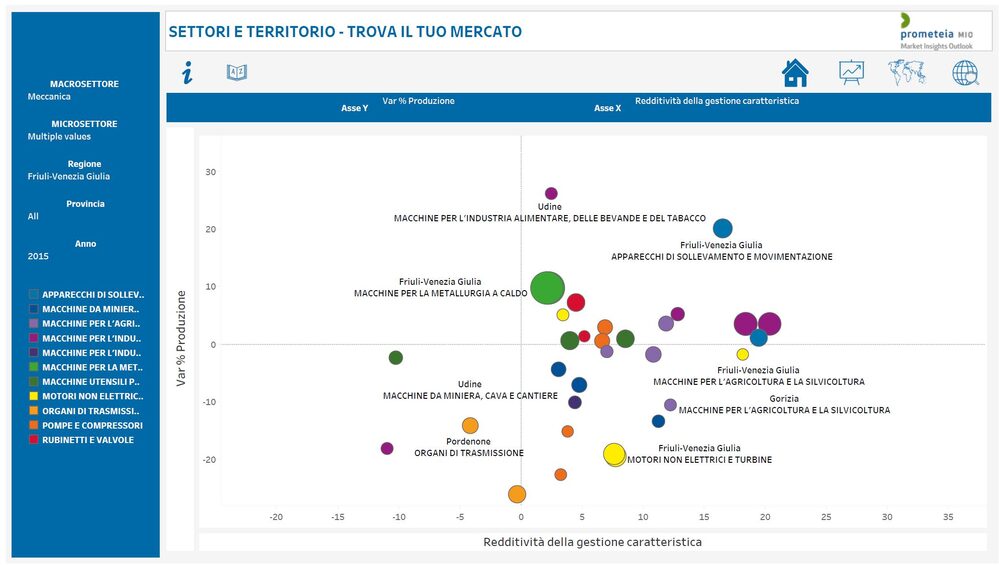

Friuli Venezia Giulia ranks among most industrialized regions in Italy, behind Piedmont and along with Veneto and Marche: the manufacturing contribution to the regional economy (2015, based on Prometeia estimates) is above 38%, thanks to a network of nearly 7000 firms, with about 97 thousands employees and a € 23.7 billion turnover.

The regional industry suffered a huge downsizing in the post-2007 years: before the crisis there were more than 11 thousands manufacturing firms employing 125 th. employees. Nevertheless, the manufacturing mission of the region has never been questioned and it continues to rely on main sectors of the Italian manufacturing model: metal products, machinery and equipment (42% of FVG industrial production in 2015), transport equipment (12%), home appliances and furniture (20%) and the “traditional” Made in Italy sectors (9%).

Waiting for the 2016 economic-financial indicators (on which we will report in next months, as soon as the balance sheets will be available), the performance analysis highlights a significant upturn in activity during 2014-15, when the growth of FVG’s industrial turnover (+9,5%) sharply outperformed (50%+) the Italian average.

However, these performance have not been reflected into corresponding increases of profits which – also squeezed by bad results of some big local players – are still suffering a relevant gap with respect the national average (in 2015, the manufacturing ROI was 2,8%, against a 7,2% national average). That points out that recovering a profitable growth path is, in the short term, a major priority for FVG companies.

In 2016, regional manufacturing exports exceeded € 13.2 billion, fueled by a further booming increase to the United States. So, in the coming months we could check if this historical record has been also reflected into an increase in margins and/or into a narrowing of the profitability gap of FVG companies.

This result would be pivotal to raise internal resources needed to face current and expected challenges for FVG firms. These challenges range from optimizing the geographical framework of their sales (the structure of regional exports is still partly mismatched to the geography of the highest potential markets), to the “4.0” alignment of B2B sectors (mechanics first) with world investment cycle current drivers (such as, infrastructure upgrading, improvement of production efficiency and sustainability). For B2C businesses, major dares are instead related with the increasing demand for distinctiveness and quality (vs quantity), “green compliance” and fair value.