Prometeia Atlante

Insight for your business

giampaolo.morittu@prometeia.com

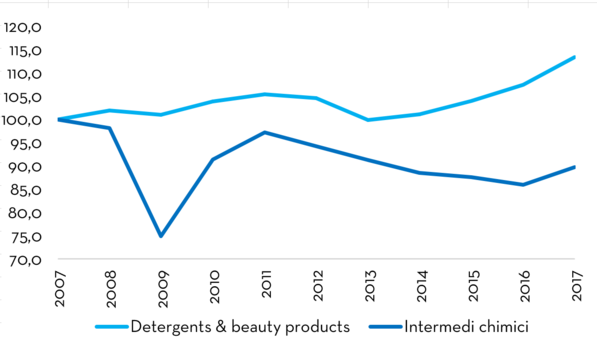

Considered for many years to be the “great sick man” of Italian manufacturing, the chemical industry is ending an overall positive 2017, which follows a decade of up and down results with a negative trend. The Italian chemical sector today counts about 700 companies and 19000 less employees than in 2007, with a 18% production gap compared to a decade ago.

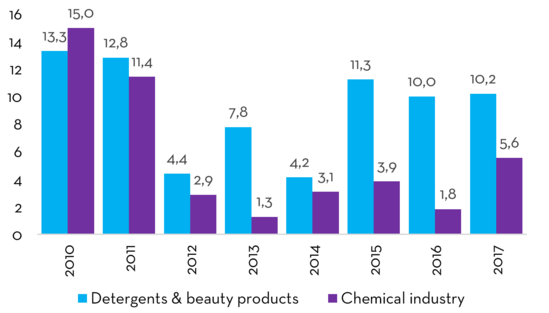

In this context, the Prometeia microsector ‘’Detergents & beauty products'' marked a sharp contrast with the overall average, showing itself as one of the most dynamic in manufacturing. About 1400 companies are currently active, employing around 27,000 employees, with 11 billion euros of production value, about 20% of chemical industry. Between 2010 and 2016 – a period marked by a steep decline of the Italian chemical business - the cosmetics and detergents turnover has grown by an average of 1%, with a significant acceleration in the last three years.

In this sector there are two distinct business segments: beauty products and detergents. Much of the progresses over recent years have been achieved thanks to the contribution of the first, due to the ability of its companies to establish themselves on the World markets. Even within the cosmetic industry, however, there are very different situations (and performances). In this sector (as in detergents industry) foreign multinational companies coexist with a large number of small and medium enterprises, often contractors for the top European players. There are also small companies active in the production of commercial brand products or niche products, mainly focused on the domestic market. This production structure, in some ways unusual in the national manufacturing, explains a large part of the foreign trade of the Italian cosmetic industry. In fact, due to the long-standing presence of multinational manufacturing plants, an increase of intra-firm trade emerged during the past years in Italy. Moreover, a large share of export could be related to the links between Italian subcontractors and multinational companies.

Following years of steady decline, since 2010 the Italian cosmetics industry has started consolidating its competitive positioning. Even if Italy’s share on world trade (around 5%, at current prices) has stabilized at a low level (particularly whether compared to that of France and Germany), the fifth position in the ranking of the world's exporters and the speed of recovery after the crisis could be considered as an important sign of vitality, particularly when considered in perspective.

However, there are still some risks in the outlook for coming years. Subcontracting relationships between Italian SMEs and large multinational companies has certainly accelerated the process of internationalization of the industry but, on the other hand, has often impaired their decision-making capacity. Therefore, in perspective the market potentials of cosmetic companies will depend on different niche products and on their abilities to conquer international markets independently while, for other companies, the growth of export is related to the improvement of the supply chain links with other top European producers.