Prometeia Atlante

Insight for your business

In the period 2018-’20, we expect a general slowdown in production dynamics that will be determined by an economic environment, which after the excellent result in 2017 (+ 1.6% real GDP), will see growth slow down (around 1% on an annual average) as a result increasing uncertainty in the domestic and international scenario.

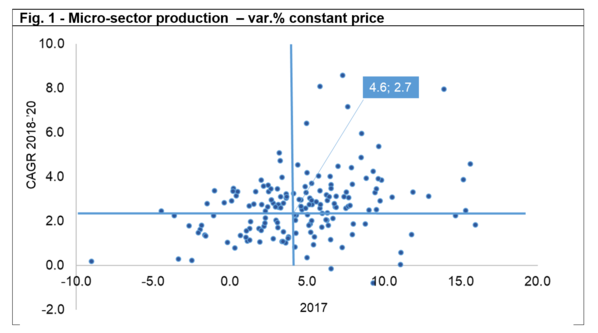

The dispersion of results remains high, with sectors growing at average yearly rates close to 10%, while others stagnate. A positive fact is that almost all the sectors are expected to grow on average for the three-year period 2018-‘20.

The dispersion graph (figure 1) shows each of the 170 Micro-sectors that divides the Italian economy. The horizontal axis shows the change in production (*) at constant prices observed in 2017 and the vertical axis shows the CAGR for the three-year period 2018-'20. First evidence is that the average growth of production (considering the simple average of the dynamics of the 170 sectors) decreased, going from + 4.6% in 2017 to + 2.7% for the next three years.

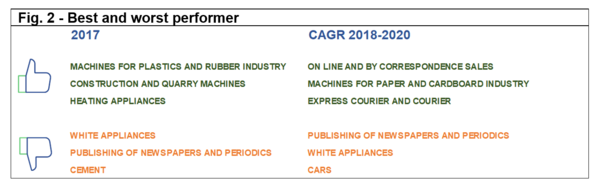

Figure 2 shows some of the sectors that are best performers (in the top 10 positions in the ranking for growth in constant price production) and worst performers (among the last 10) in the two periods considered.

In 2017, manufacturers of machines for the plastic and rubber industry are among the winners and are supported by the presence of incentives and by dynamism of user sectors, mainly the automotive one. The production of mining, quarrying, and construction machinery is increasing after undergoing significant fall in previous years. The recovery signals the awakening of national construction, partly due to the presence of incentives for the redevelopment of buildings.

In the transition to the three-year forecast period, among the winners it is interesting to note that, in a context of generalized slowdown in the manufacturing industry, the sectors linked to the development of on-line commerce will grow more. E-commerce will also support the paper and cardboard machinery industry, thanks to the growth of ecological packaging, which will allow a recovery of the sector after years of heavy decline following the publishing crisis.

While white appliances continue to suffer, small-appliances (especially heating appliances manufactures) will improve on excellent results of 2017, supported by the transition to high efficiency products.

The publishing industry, which competes with on-line information, continues to suffer. In 2017, the production of cement companies is still contracting, but is no more on the worst performers list for 2018-'20, thanks to the expected recovery for investments in construction. In the lower part of the classification also figures the Micro-sector of automobiles: after a period of strong growth, it will pay the decisive slowdown in domestic demand.