Prometeia Atlante

Insight for your business

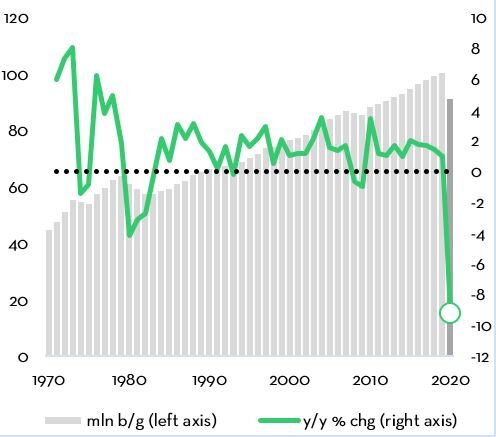

U.S. oil price crashes into negative territory for first time in history. The enthusiasm for 10 million b/g of cuts announced at the beginning of April by the Opec+ countries quickly evaporated in the face of the harsh reality of an oil demand expected to fall by more than 30 million b/g in April alone, paving the way for the worst y/y fall of the last 50 years (fig 1).

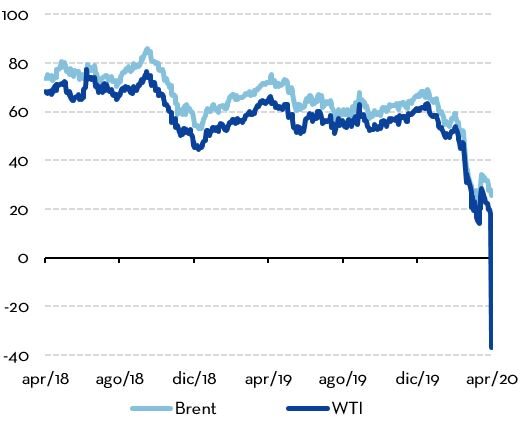

After rising above $34 b/b. at the beginning of the month, Brent retrenched again to $20 b/b in the third week of the month, while West Texas Intermediate (WTI) first forward position even fell in negative territory in the night of the 20th of April (fig 2). Negative prices means that the owner of a long position in oil would have to pay someone else to take that oil off his hands. How could it have happened?

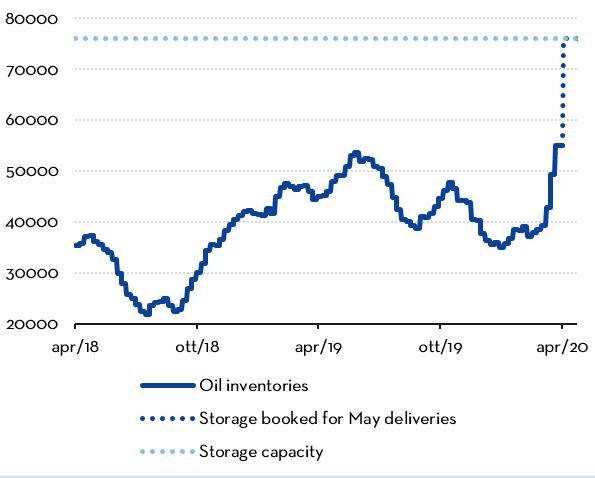

Without digging too much into technicalities, whilst the Brent contract is cash-settled, as the Nymex WTI contract expires a quantity of oil is converted into physical barrels that either need to be consumed or stored at the Cushing (Oklahoma) delivery point. This occurs under normal circumstances. However, due the exceptional situation generated by the effects of the Covid-19 containment measures, the collapse in refinery demand has led to the accumulation of a huge amount of unsold oil, filling the tanks to the brim. With little or no storage left to lease, market participants who had not yet settled their position on April 20 (the May delivery deadline) found themselves squeezed between a rock and a hard place. Forced to liquidate their positions, they rushed for the door to avoid taking physical delivery of crude, willing to pay up to $37/b. in order to get rid of their “long” contracts.

What happened between 20 and 21 April can therefore be catalogued as an exceptional event, never occurred before and for the most part justified by technical factors (or inexperienced investors behavior). Even then, it would be simplistic to equate it to a temporary aberration of the market. Indeed, the lack of storage space in Cushing point to an imbalance between supply and demand far wider than expected, meaning that the restrictive measures had a much more profound impact than assumed just a few days ago. This opens up to new, pressing questions both for the immediate management of the crisis and for the medium term exit strategy. This is an issue which not only involves the commodity markets, (specifically the oil market) but also many other economic sectors.

Saving at all costs or adapting to the market laws? The first question concerns the availability of adequate instruments to deal with the consequences of the crisis or, for what regards the United States oil industry, the scope for the US administration to keep the shale oil industry safe from the inevitable chain failures to which, ceteris paribus, this sector is doomed to. Forced to deal with breakeven prices above $35/b and $40 billion maturing debt in the next three years, it is indeed a matter of weeks, not months, for many upstream companies to file, en masse, the Chapter 11 bankruptcy given the current sub-20 $/b environment. A challenge made more pressing by the upcoming November election deadline, to which the Trump administration has so far failed to respond adequately.

The depletion of storage space is, in fact, clear evidence of how the production cut promoted at the beginning of April came too little and too late to cope with a double-digit drop in consumption. Moreover, no much relief is likely to come from both the promises to impose a sort of duty on crude oil imported from Saudi Arabia (weighting less than 6% on total US imports) and the replenishment of strategic stocks (SPR), whose absorption rates represent a fraction of the daily drop rate of demand observed in recent weeks. The U.S. administration could intervene through the injection of public capital in the company balance sheets, even though the effectiveness of this strategy is conditional on the duration and on the shock. Will the Coronavirus lead to a structural review of fuel consumption, what would be the economic sense of keeping a sector producing far more oil than the market needs alive? A dilemma that closely affects the oil market but, by similarity, involves other important sectors heavily hit by the lockdown consequences, such as the aviation and rails.

What awaits us after the emergency phase? Timing of the exit from the emergency and start of Phase 2 will be critical to anticipate the future direction of oil prices. Equally decisive will be an early reading of the scars left by the pandemic disease on the future growth patterns. In order to avoid a new, large-scale wave of pandemic, a recently published study in the journal Science [1] anticipates the need for policymakers to promote a certain degree of social distancing at least until 2022. Net of a rapid discovery of an effective cure/vaccine, this will likely keep on affecting, consciously or not, the attitudes of consumers and businesses well beyond the end of the most acute phase of the emergency, thus rooting some behaviors implemented in the last two months. For example, it is easy to imagine a future in which the individual means of transport will be favored over the collective means of transport but where, at the same time, the traditional work will shift from the traditional open spaces to a more evolved form of smart working. We are not going to dive into the analysis of the trade-off between the higher gasoline consumption associated with the former scenario and the lower of the latter. However, we want to emphasize that the Covid-19 traces are likely to stay far beyond the most acute phase of the crisis, making it inevitable to adapt the current economic model to the changing choices of consumers and businesses.

What will last of the pre-Covid19 trends? In recent years, the fight against environmental pollution has been one of the most important drivers of the policy choices in Europe: think of the regulations to reduce CO2 emissions, whose effects directly mirrored (via lower energy consumption) on oil demand, contributing to curb its growth path and encouraging the transition to a more sustainable development model. These efforts risk being lost in a scenario in which the reduction in the funds raised to promote the green transition will be associated to the lower attractiveness of alternative forms of transport due to lower gasoline costs. The risk is that, although not completely shelved, energy transition will shift to the background of policymakers' agenda. Although apparently justified by the exceptionality of the historical moment, this would nevertheless be a short-sighted strategy: as recently published study by Prometeia evidence, a fiscal stimulus focused in green investments could indeed generate a growth path higher than the existing one, while anticipating carbon neutrality goal by at least five years.

To sum up, the depletion of oil storage space in North America, of which negative prices are the direct consequence, gives a measure of the pervasiveness of the shock caused by the distancing measures on the energy raw materials markets. Here we have highlighted three aspects that, of course, represent only a small portion of the myriad of issues associated to the economic impact of the lockdown. Task of policymakers and companies – now and in the coming months -will be to lead the way out of the crisis by rethinking the current development model. In other words, balancing between opportunities and risks of an economic and social environment that, as the dynamics of oil prices and inventories suggest, will be affected by the lockdown consequences for much longer than initially expected.