Prometeia Atlante

Insight for your business

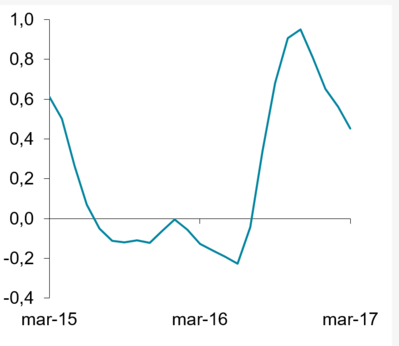

The latest information on activity levels confirms a consolidated recovery of the Italian manufacturing sector in the first months of 2017, albeit with some indications of cyclical downturn. The data provided by Istat on the January-March quarter show a significant rise in the overall turnover year on year (+6.1% in terms of value, +4.6% in volume). This is a slight deceleration compared to the previous months, a physiological slowdown given the strong rebound in production activity registered in the second half of last year.

Although data are still extremely partial, these results are generally compatible with the 1.6% volume increase estimated for manufacturing in 2017 (Industrial Sector Analysis report Prometeia-Intesa Sanpaolo, May 2017).

At the sectoral level, in the first quarter 2017 13 sectors out of 15 are expanding, against 9 in 2016. The recent economic evolution highlights a more sustained growth compared to the assumptions incorporated in our scenario for intermediate goods (basic metals, metal products, intermediate chemicals, construction materials) and the electrical equipment sector. The strong expansion recently registered by the orders in machinery and equipment sector – both in the domestic market (that benefits from the Super and Hyper amortisation effect in support of the production system renewal cycle) and in the international markets – could open up new perspectives for a more intense strengthening also for this segment. Conversely, the evolution of detergents and beauty, computer and electronics and furniture lags below expectations.