Prometeia Atlante

Insight for your business

Maria

Civita Cafolla, Simone Lauretti, Daniele Blanco, Giulia Pallini, Letizia

Ercolani

Significant increase in non-performing loans exposure, limited barriers to entry, opportunities provided by the devaluation of the Turkish Lira for operators able to get financed in strong currencies (at least in the short term) lead to believe there will be a considerable development of the Turkish Asset Management Companies (‘AMCs’) sector, with potential entry opportunities for foreign players.

Turkey’s lending market has been growing since 2001, mainly driven by macroeconomic growth, stabilizing inflation, portfolio inflows and government initiatives.

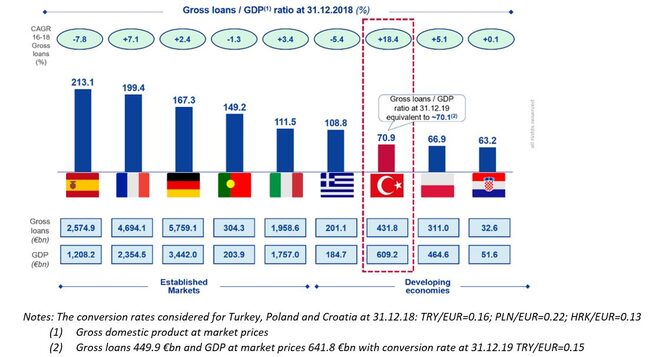

Compared to established economies such as Italy, France, Germany and Spain, Turkey shows higher lending market growth rates. Moreover, a ratio between gross loans and GDP in Turkey still around 70% in 2019 suggests a further potential, compared to the much higher ratios of more mature economies (from Italy’s 111.5% to Spain’s 213.1%).

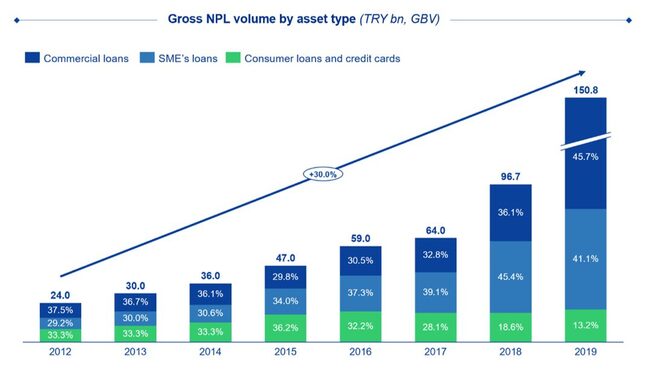

As the credit market grew, the stock of non-performing loans has increased significantly over the past few years, with a growing weight of commercial and Small and Medium Enterprises (“SMEs”) NPLs (CAGR 2012-2019 of +30%).

On one hand, the restrictions imposed on customer spending (for instance, a limit on credit cards and consumer loans) have put a brake on loan growth of loans to retail customers, which are normally more secured than corporate and commercial loans.

On the other hand, the measures implemented to grant liquidity to corporates, especially SMEs – such as the Credit Guarantee Fund, established in 1993 but stayed idle until 2017 (totally up to TRY 250 billion in guarantees in 2017) – contributed to simultaneously increase corporate loans volumes.

The aforementioned change in portfolios composition has certainly played a key role in the deterioration of the asset quality of Turkish banks.

At the end of 2019, gross non-performing loans amount to TRY 150.8 billion (roughly EUR 22.6 billion, conversion rate TL/EUR 0,15), equal to 5.7% of total loans: 45.7% are represented by commercial loans while 41.1% by loans to SMEs.

Despite the increasing amount of NPLs in bank credit portfolios, the percentage of their disposal is not significant compared to the gross stock and the recovery ratio shows room for improvement (21.1% at the end of 2019, down by 14 percentage points compared to the previous year).

The large amounts of impaired loans deriving from the 2001 Turkish banking crisis triggered the need of finding a practical solution to manage such credits. In November 2006, after the enactment of the regulation governing the foundation and operations of NPL servicing platforms, the so-called Asset Management Companies (‘AMCs’), financial institutions in Turkey started consistently selling non-performing loans to AMCs. Since then, the NPL purchasing market has experienced considerable growth, with an increasing number of banks selling portfolios, as well as banks selling larger portfolios and the entry of new AMCs in the market.

The major driving factors behind this growth were, firstly, that banks and other financial institutions realized the benefits of selling NPLs (which allowed to avoid operational costs and reduce NPL ratios, hence being able to focus on their core business) and, secondly, the increasing maturity and sophistication of AMCs in the market, which improved the effectiveness of recovery policies.

The Banking Regulation Supervisory Authority (BRSA) has never created barriers for market entrants. However, NPL AMCs are now required to maintain a minimum level of share capital, equal to TRY 20 million. Moreover, the 2017 legislation that has authorized AMCs to manage state-owned banks NPL portfolios has been and will be a positive driver of growth for the sector. Nowadays, the state banks active in the Turkish banking system are three, with total assets amounting to TRY 1,508.7 billion (36.8% of total) and total loans up to TRY 1,044.5 billion (40.6% of total). These three banks are flanked by three investment banks, eight local private banks and nine foreign private banks.

Since the NPL AMC sector is characterized by intense competition, an aggregation process among the main AMCs is already in place, in order to achieve significant market shares and better manage the significant growth of volumes of the NPL servicing market.

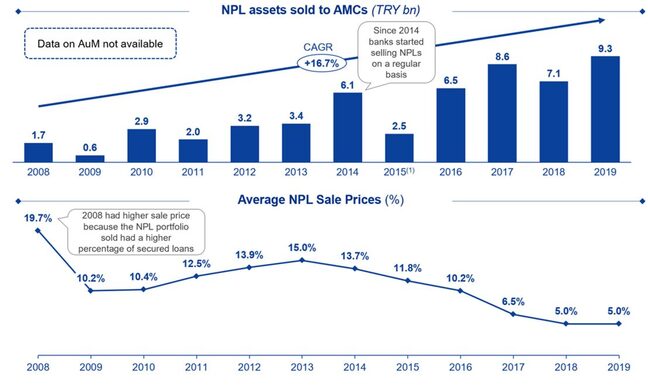

The amount of NPLs sold to AMCs has kept increasing with an annual growth rate of around 17%, reaching TRY 9.3 billion in 2019.

At the beginning sale prices were high mainly because of the higher percentage of secured loans sold. After trending upwards until 2013, with the entrance of new players and the set-up of M&A operations among incumbents, NPL sales prices have declined, on average, from 15% to 5% of the face value. This reduction is mainly due to the lower quality of NPL portfolios for sale and the increasing funding costs of AMCs.

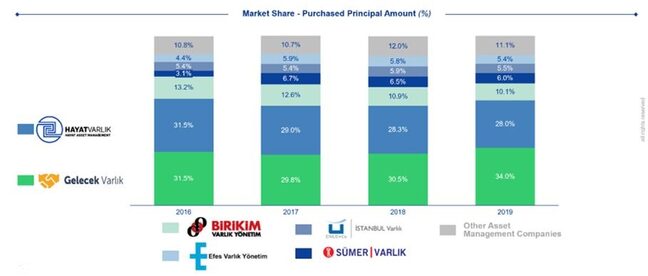

Currently the AMC market is composed of 20 players, to which TRY 9.3 billion of NPL assets were sold in 2019. We estimate a further market growth, because of the growing non-performing component of the bank credit portfolios and the consequent need to reduce it. The NPL servicing market is mainly concentrated in the first six AMCs, which hold about 89% of the market. In particular, the first two companies have purchased nearly 60% of the total.

Within this competitive context, there is room for a considerable development of the AMCs sector.

In light of increasing NPL volumes observed in the last years, and all the more so after the recession caused by COVID-19 and its subsequent lockdown, it is likely that this trend will continue in the next future. The new regulation introduced in 2017 allowing AMCs to buy and manage loan portfolios from state-owned banks will also represent a positive driver for the sector, just like in the past few years.

The Turkish regulator is also planning to establish an AMC jointly owned by the Turkish banks. Such an AMC is expected to invest heavily on energy and construction industry-related bad debts. It is conceivable that the regulation will further support AMCs in order to underpin this initiative. The long-term objective will be the securitization of NPLs, which is a common model in the EU, but is not yet feasible by law in Turkey.

In addition, the significant increase in NPLs in the upcoming period will make it easier for new entrants, given the absence of entry barriers and a single minimum share capital requirement for AMCs of only TRY 20 million. In particular, significant opportunities can be exploited for players able to be funded by strong currencies financing, thus leveraging on the devaluation of the Turkish Lira.